5 Musts Before Buying a Home

About Redlands Realty & Loan believes buying a home is still one of the best decisions you can make. But are you prepared? Here are a few things to consider.

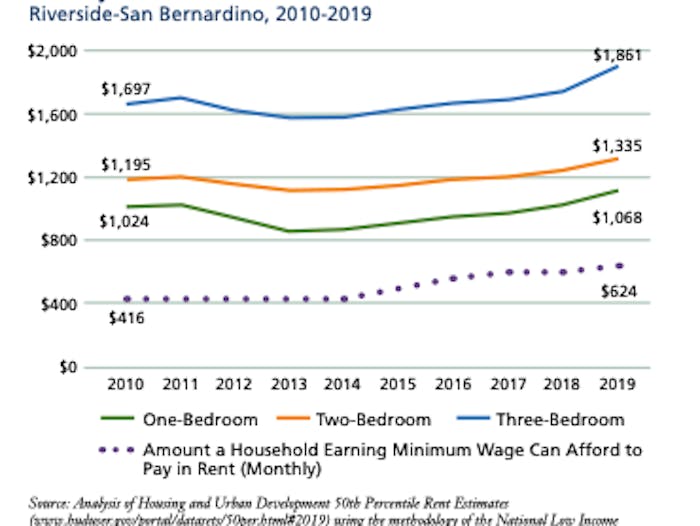

There are many reasons why you should consider owning – instead of renting – your home. Tax benefits, the pride of ownership… When renting, you're almost guaranteed to pay more every year (see chart below for a Riverside-San Bernardino example). But owning your home locks you into a fixed monthly payment until it’s paid off, while adding a real asset as part of your long-term investments.

Source: San Bernardino County Transportation Association

Real assets/properties can also increase in value over time. The current national average increase is about 6%, which can add roughly $6,000 per $100,000 value of your home every year. If you continue making payments on time (so you pay down the principal) then you’re on your way to saving money and kick-starting your financial security. However, before buying a home, here are five (5) MUSTs that we recommend for you to consider:

MUST manage your credit score

Credit is used by the lender to identify your worthiness to repay the loan and make on-time payments. Generally, a 620 credit score is needed; but if your score is less than that, there are loans still available but you’ll need more cash as a down payment. The major three (3) bureaus - Equifax, Transunion, and Experian - keep track of your transactions referring to credit, and allow you to get a free credit report once every twelve (12) months. You can visit annualcreditreport.com or call 1-(877)-322-8228 to get your free copy of your credit report.

MUST understand the costs of buying a home

This is a life-changing decision – and there isn’t any reason to pay more than is required to close the deal. Understanding the real costs will help you feel empowered/more confident about the transaction. When buying a house, there are several parties involved: the appraiser, lender, title, escrow, loan originator, real estate agent… and everyone is paid and should be. These professionals make buying real estate a less scary task and have your best interest in mind. How much does it cost? The average purchase of a home will cost a total between 2-3% of the sales price. That percentage changes, being higher for low loan amounts and lower for high loan amounts.

MUST do location research

Location is extremely important! The loan amount you qualified for will often identify the areas available for you. However, make sure to take note of important factors (commuting costs, school district, etc.) for you and your family for at least 3 years (preferably more). In most of cases, this is the minimum amount of time before homeowners can upsize and/or sell your property for more than you paid for.

Source: Our own property search tool, shows available homes in Redlands on May 18, 2020

MUST consider getting pre-approved

Before developing criteria to give to your real estate agent, we strongly suggest for you to get pre-approved for financing. Now don't let that scare you, your mortgage broker is a dedicated professional with secure systems - so none of your personal financial information will get out to the public! Once qualified, you'll be able to shop homes with confidence that you'll be able to present an offer and know the money will be there to close on time.

MUST gather a down payment

But how much do you need as a down payment? Great question. If you have money, great; having a downpayment will help keep the interest rate down. But if you do not have any money, you may qualify for one of the many Down Payment Assistance loans offered by the state, county, or city. These loans generally offer a second mortgage which usually does not need to be repaid after a few years, however, nothing is free. These programs usually lead to higher interest in your first mortgage than any other options. But frankly, if you don’t have any money and they are willing to help, you are still much better off with a slightly higher rate in a home you own than if you continue to rent.

Now, it’s time to set your goals. Before you know it you’ll be living in your beautiful, new home and creating wealth. Maintain a stable payment and have pride in being able to call yourself a homeowner. If you have any questions, please feel free to contact us and we’ll take care of you.